According to the FBI, more than one million burglaries are committed in the United States each year, with victims suffering an estimated $3 billion in combined property losses.1 Fortunately, there are some proven tactics you can use to decrease your likelihood of a home invasion.

Most burglars won’t go to extreme lengths to enter a residence. They are looking for easy access with minimal risk. A monitored security system can be an effective deterrent—homes without one are 300% more likely to be burglarized—but it isn’t the only way to protect your property.2 The strategies below can help to maximize your home’s security and minimize your chances of being targeted by intruders. Thinking about listing your home? We have some additional recommendations for you. Contact us to find out the procedures we use to keep our clients and their property safe and secure during the buying and selling process.

A steel door is generally considered the strongest, but many homeowners prefer the look of wood. Whatever material you choose, make sure it has a solid core and pair it with a Grade 1 or 2 deadbolt lock with a reinforced strike plate.4

Aftermarket window locks are an easy and inexpensive upgrade that can provide an additional layer of protection for your home. Choose a lock that is compatible with your window frame material and a style that is appropriate for the window type. And consider using a specialty film on windows that are adjacent to a door. Security film holds shattered glass in place, making the windows more difficult to penetrate.5 2. Landscape for Security When it comes to outdoor landscaping, many of us think about maintenance and curb appeal. But the choices we make can impact our home’s security, as well. Thieves target homes that they can enter and exit without being detected. Here are a few tweaks that can make your property less appealing to potential intruders.

A privacy hedge may keep out nosy neighbors, but it can also welcome thieves—so trim overgrown trees and shrubs that obstruct the view of your property. According to police officers, they offer an ideal environment for criminals to hide.6

Don’t eliminate shrubbery altogether, though. Certain hedges can actually offer a deterrent to robbers. Plant thorny rose bushes or sharp-leaved holly beneath your first-story windows for both beauty and protection. Add some loose gravel that crunches when disturbed. 3. Light Your Exterior When it’s dark outside, criminals don’t need to rely on overgrown shrubbery to hide. Luckily, a well-designed outdoor lighting system can make your home both safer and more attractive.

Eliminate pockets of darkness around your yard and home’s perimeter with strategically placed outdoor lights. Use a combination of flood, spot, well, and pathway lights to add interest and highlight natural and architectural details.

The soft glow of landscape lighting isn’t always enough to dissuade a determined intruder. But a motion-activated security light may stop him in his tracks. And if you choose a Wi-Fi connected smart version, you can receive notifications on your phone when there’s movement on your property. 4. Make It Look Like You’re Home Motion-activated lights aren’t the only way to make an intruder think you’re at home. New technology has made it increasingly possible to monitor your home while you’re away. This is especially important since most burglaries take place on weekdays between 10 am and 3 pm, when many of us are at work or school.2

A survey of convicted burglars revealed that the majority avoid breaking into homes if they can hear a television or if there’s a vehicle parked in the driveway.7 If you’re away from home, try connecting your TV to a timer or smart plug. And when you travel, leave your car out or ask a neighbor to park theirs in your driveway.

In that same survey, every respondent said they would knock or ring the doorbell before breaking into a home. A video doorbell not only alerts you to the presence of a visitor, it also enables you to see, hear, and talk with them remotely from your smartphone—so they’ll never know you’re gone. 5. Keep Valuables Out of Sight Few home invasions are conducted by criminal masterminds. In fact, a survey of convicted offenders found that only 12% planned their robberies in advance, while the majority acted spontaneously.8 That’s one of the reasons security experts caution against placing valuables where they are visible from the outside.9

Don’t tempt robbers with a clear view of the most commonly stolen items, which are cash (think purses and wallets), jewelry, electronics, firearms, and drugs (both illegal and prescription).6 Take a walk around your property to make sure none of these items are easily visible.

Consider the possessions that are on display inside your home, as well. It’s always a good idea to lock up firearms, sensitive documents, and expensive or irreplaceable items when you have housekeepers or other service providers on your property. 6. Highlight Your Security Measures While it’s prudent to hide your valuables, it’s equally important to advertise your home’s security features. In surveys, convicted burglars admit to avoiding homes with obvious protective measures in place.7,8

Security cameras are the most common home protection device and for good reason.10 Not only do they help prevent crime (burglars are known to avoid them), they can offer peace of mind for homeowners who want to sneak a peek at their property while away.11 And if you do experience a break-in, security camera footage can help police identify your intruder.

Security system placards and beware-of-dog signs are also shown to be effective deterrents.8 Of course, you should back up your threats with a noisy alarm and loud barking dog for maximum impact. 7. Limit What You Share on Social Media Social media platforms can be a great way to stay connected with friends and family, but it’s easy to reveal more than you’ve intended. Be thoughtful about what you’re posting—and who has access.

It can be tempting to upload a concert selfie or pictures from your beach vacation. But these types of photos scream: “My house is unoccupied!” Try to wait until you’ve returned home to share the photos on social media.

Think twice about connecting with strangers or casual acquaintances on social media. If you enjoy sharing family updates and personal photos, it’s safer to limit your followers to those you truly know and trust. YOUR HOME IS SAFE WITH US We take home security seriously. That’s why we have screening procedures in place to keep our clients and their homes safe when they are for sale. We also remind our buyers to change the locks before they move into their new homes and provide referrals to locksmiths and home security companies that can help. To learn more about our procedures and how you can stay safe during the buying and selling process, contact us to schedule a free consultation! Sources:

Selling your home when you still need to shop for a new one can feel daunting to even the most seasoned homeowner––especially when the demand for new homes keeps rising, but the supply feels like it's dwindling.¹ You're not alone either if you're already feeling drained by the complex logistics of trying to sell and buy a new home all at once.

Searching for a new home can be exciting, but many homebuyers admit that it can also be stressful, especially if you live in an unpredictable market with plenty of competitors. Unfortunately, waiting out a competitive housing market isn’t always the best idea either since listings are expected to remain limited in the most coveted neighborhoods for some time.² That doesn't mean, though, that you should just throw up your hands and give up on moving altogether. In fact, as a current homeowner, you could be in a better position than most to capitalize on a seller’s market and make a smooth transition from your old home to a new one. We can help you prepare for the road ahead and answer any questions you have about the real estate market. For example, here are some of the most frequent concerns we hear from clients who are trying to buy and sell at the same time. “WHAT WILL I DO IF I SELL MY HOUSE BEFORE I CAN BUY A NEW ONE?” This is an understandable concern for many sellers since the competitive real estate market makes it tough to plan ahead and predict when you'll be able to move into your next home. But chances are, you will still have plenty of options if you do sell your home quickly. It may just take some creativity and compromise. Here are some ideas to make sure you're in the best possible position when you decide to list your home: Tip #1: Flex your muscles as a seller. In a competitive market, buyers may be willing to make significant concessions in order to get the home they want. In some cases, a buyer may agree to a rent-back clause that allows the seller to continue living in the home after closing for a set period of time and negotiated fee. This can be a great option for sellers who need to tap into their home equity for a downpayment or who aren’t logistically ready to move into their next home. However, many lenders limit the duration of a rent-back to 60 days, and there are liability issues to consider before entering into an agreement. A contract and security deposit should be in place in case of any property damage or unexpected repairs that may be needed during the rent-back period.³ Tip #2: Open your mind to short-term housing options. While it can be a hassle to move out of your old home before you’re ready to move into your new one, it’s a common scenario. If you’re lucky enough to have family or generous friends who offer to take you in, that may be ideal. If not, you’ll need to find temporary housing. Check out furnished apartments, vacation rentals and month-to-month leases. If space is an issue, consider putting some of your furniture and possessions in storage. You may even find that a short-term rental arrangement can offer you an opportunity to get to know your new neighborhood better—and lead to a more informed decision about your upcoming purchase. Tip #3: Embrace the idea of selling now and buying later. Instead of stressing about timing your home sale and purchase perfectly, consider making a plan to focus on one at a time. Selling before you’re ready to buy your next home can offer a lot of advantages. For one, you’ll have cash on hand from the sale of your current home. This will put you in a much better position when it comes to buying your next home. From budgeting to mortgage approval to submitting a competitive offer, cash is king. And by focusing on one step at a time, you can alleviate some of the pressure and uncertainty. “WHAT IF I GET STUCK WITH TWO MORTGAGES AT THE SAME TIME?” This is one of the most common concerns that we hear from buyers who are selling a home while shopping for a new one, and it’s realistic to expect at least some overlap in mortgages. To make sure you don't get into a situation where you are carrying dual mortgages for longer than you can afford, examine your budget and calculate the maximum number of months you can afford to pay both.⁴ If you simply can’t afford to carry both mortgages at once, then selling before you buy may be your best option. (See Tip #3 above.) But if you have some flexibility in your budget, it is possible to manage both a home sale and purchase simultaneously. Here are some steps you can take to help streamline the process: Tip #4: As you get ready to sell, simplify. You can condense your sales timeline if you only focus on the home renovations and tasks that matter most for selling your home quickly. For example, clean and declutter all of your common areas, refresh your outdoor paint and curb appeal, and fix any outstanding maintenance issues as quickly as possible. But don't drain unnecessary time and money into pricey renovations and major home projects that could quickly bog you down for an unpredictable amount of time. We can advise you on the repairs and upgrades that are worth your time and investment. Tip #5: Prep your paperwork. You'll also save valuable time by filing as much paperwork as possible early in the process. For example, if you know you'll need a mortgage to buy your next home, get pre-approved right away so that you can shorten the amount of time it takes to process your loan. Similarly, set your home sale up for a fast and smooth transition by pulling together any relevant documentation about your current home, including appliance warranties, renovation permits, and repair records. That way, you're ready to provide quick answers to buyers' questions should they arise. Tip #6: Ask us about other contingencies that can be included in your contracts. Part of our job as agents is to negotiate on your behalf and help you win favorable terms. For example, it’s possible to add a contingency to your purchase offer that lets you cancel the contract if you haven't sold your previous home. This tactic could backfire, though, if you're competing with other buyers. We can discuss the pros and cons of these types of tactics and what’s realistic given the current market dynamics. “WHAT IF I MESS UP MY TIMING OR BURN OUT FROM ALL THE STRESS?” When you're in the pressure cooker of a home sale or have been shopping for a home for a while in a competitive market, it's easy to get carried away by stress and emotions. To make sure you're in the right headspace for your homebuying and selling journey, take the time to slow down, breathe and delegate as much as possible. In addition: Tip #7: Relax and accept that compromise is inevitable Rather than worry about getting every detail right with your housing search and home sale, trust that things will work out eventually––even if it doesn't look like your Plan A or even your Plan B or Plan C. Perfecting every detail with your home decor or timing your home sale perfectly isn't necessary for a successful home sale and compromise will almost always be necessary. Luckily, if you've got a good team of professionals, you can relax knowing that others have your back and are monitoring the details behind the scenes. Tip #8: Don't worry too much if your path is straying from convention Remember that rules-of-thumb and home-buying trends are just that: they are estimates, not facts. So if your home search or sale isn't going exactly like your neighbor’s, it doesn't mean that you are doomed to fail. It's possible, for example, that seasonality trends may affect sales in your neighborhood. So a delayed sale in the summer or fall could affect your journey––but not necessarily. According to the National Association of Realtors, the housing market tends to be more competitive during the summer and less competitive during the winter.⁵ But it's not a hard and fast rule, and every real estate transaction is different. That's why it's important to talk to a local agent about your specific situation. Tip #9: Enlist help early. Which leads us to our final tip: If possible, call us early in the process. We'll not only provide you with key guidance on what you should do ahead of time to prepare your current home for sale, we'll also help you narrow down your list of must-haves and wants for your next one. That way, you'll be prepared to act quickly and confidently when it’s time to list your house or make an offer on a new one. It's our job to guide you and advocate on your behalf. So don't be afraid to lean on us throughout the process. We’re here to ease your burden and make your move as seamless and stress-free as possible. BOTTOMLINE: COLLABORATE WITH A REAL ESTATE PROFESSIONAL TO GET TAILORED ADVICE THAT WORKS FOR YOU Buying and selling a home at the same time is challenging. But it doesn't have to be a nightmare, and it can even be fun. The key is to educate yourself about the market and prepare yourself for multiple scenarios. One of the best and easiest ways to do so is to partner with a knowledgeable and trustworthy agent. A good agent will not only help you evaluate your situation, we will also provide you with honest and individually tailored advice that addresses your unique needs and challenges. Depending on your circumstances, now may be a great time to sell your home and buy a new one. But a thorough assessment may instead show you that you're better off pausing your search for a while longer. Contact us for a free consultation so that we can help you review your options and decide the best way forward. Sources:

It’s the old supply-and-demand predicament: U.S. home sales continue at a rapid pace, but the number of listings remains limited. Amid historically low mortgage rates, buyers keep shopping, reducing inventory and sparking a rise in home prices.

Meanwhile, homebuilders are coping with an increase in material costs and a shortage of labor. These issues come during an ongoing housing shortage. A National Association of Realtors study shows the U.S. has a deficit of about 2 million single-family homes and 3.5 million other housing units.[1] Follow along to learn the five factors that illustrate where the U.S. housing market is today and is heading tomorrow. ROCK-BOTTOM MORTGAGE RATES TO GRADUALLY RISE Low interest rates continue to fuel demand from homebuyers. Some experts believe mortgage rates will creep up later this year, but they expect rates to remain near historic lows.[2] In June, the Mortgage Bankers Association reported that 2020 closed with the average rate for a 30-year, fixed-rate mortgage at 2.8%. But the association anticipates the average rate climbing to 3.5% at the end of 2021 and 4.2% by the end of 2022.[3] What does it mean for you? When mortgage rates are at or near historic lows (as they are today), you should seriously consider taking advantage of those rates to borrow money for a home purchase or to refinance your existing mortgage. HOME PRICES EXPECTED TO KEEP CLIMBING In June, the national median list price for a home reached an all-time high of $385,000, up 12.7% on a year-over-year basis.[4] And according to the Home Buying Institute, various reports and forecasts indicate home prices will keep climbing throughout 2021 and into 2022.[5] While this may be welcome news for homeowners, high prices are pushing homeownership out of reach for a growing number of first-time buyers. What does it mean for you? If you’re a buyer waiting on the sidelines for prices to drop, you may want to reconsider. While the pace of appreciation should taper off, home prices are expected to continue climbing. And rising mortgage rates will make a home purchase even more costly. SINGLE-FAMILY HOME SALES REMAIN ROBUST Single-family home sales are down from their peak in October 2020 yet are still above the overall level last year. In May 2021, 5.8 million existing single-family homes were sold in the U.S. That’s a 45% increase over the 4 million homes sold in May 2020.[6] However, home sales saw a 0.9% dip in May 2021 compared with the previous month, the National Association of Realtors says. That was the fourth straight month for a decline in home sales. The number of home sales has slid recently because of rising prices and a lack of inventory, but Fannie Mae expects total home sales to tick up slightly in the fourth quarter and finish the year up 3.8% over last year.[6,7] What does it mean for you? The market for single-family home sales remains quite active. As a result, if you’re a homeowner, you may want to ponder whether to sell now, even if you hadn’t necessarily been thinking about it. With demand high and inventory low, your home could fetch an eye-popping price. LACK OF INVENTORY STILL CONSTRAINS THE HOME MARKET According to the National Association of Realtors, in May there were 1.23 million previously owned homes on the market, down 20.6% from the same time last year.[6] This translates to a 2.5-month supply of homes, which is well below the 6 months of inventory typical in a balanced market.[6,8] According to the Realtors group, the lack of inventory translates into tougher searches for buyers and contributes to a rise in prices.[6] What does it mean for you? If you’re thinking of selling your home, now may be the right time to do it. Across the country, it’s a seller’s market, meaning demand is outpacing supply. That supply-and-demand imbalance puts sellers in a great position to sell their homes at a premium price. The May 2021 Realtors Confidence Index from the National Association of Realtors found the average home that was sold attracted five offers, and the association says nearly half of homes are selling above list price.[9,10] CONSTRUCTION OF SINGLE-FAMILY HOMES SEES SLIGHT UPTICK Frustrated buyers may soon find some relief from an increase in new construction. Economists forecast that 1.1 million new houses will be started in 2021, compared with a predicted 940,000 units just six months ago, with 1.2 million new starts predicted for 2022 and 2023, according to the Urban Land Institute.[11] What does it mean for you? Given the issues affecting the new-home market, it may make sense to widen your home search to include both new and existing homes. Your brand-new dream home may not be available, but you might be able to find an existing home that lives up to your vision. Keep in mind that we can help you find either a new or existing home and can advocate for you to ensure you get the best deal possible. ARE YOU THINKING OF BUYING OR SELLING? If you’re in the market for a home, you’re ready to sell your house or you’ve simply been wondering whether you should sell, you could benefit from an expert to help you navigate the hot real estate market. Let’s set up a free consultation to discuss your situation. We can review your options and come up with a plan to capitalize on the value of your current property or to find your ideal next home. Sources:

If you’re searching for drama, don’t limit yourself to Netflix. Instead, tune in to the real estate market, where the competition among buyers has never been fiercer. And with homes selling for record highs,1 the appraisal process—historically a standard part of a home purchase—is receiving more attention than ever.

That’s because some sellers are finding out the hard way that a strong offer can fizzle quickly when an appraisal comes in below the contract price. Traditionally, the sale of a home is contingent on a satisfactory valuation. But in a rapidly appreciating market, it can be difficult for appraisals to keep pace with rising prices. Thus, many sellers in today’s market favor buyers who are willing to guarantee their full offer price—even if the property appraises for less. For the buyer, that could require a financial leap of faith that the home is a solid investment. It also means they may need to come up with additional cash at closing to cover the gap. Whether you’re a buyer or a seller, it’s never been more important to understand the appraisal process and how it can be impacted by a quickly appreciating and highly competitive housing market. It’s also crucial to work with a skilled real estate agent who can guide you to a successful closing without overpaying (if you’re a buyer) or overcompensating (if you’re a seller). Find out how appraisals work—and in some cases, don’t work—in today’s unique real estate environment. APPRAISAL REQUIREMENTS An appraisal is an objective assessment of a property’s market value performed by an independent authorized appraiser. Mortgage lenders require an appraisal to lower their risk of loss in the event a buyer defaults on their loan. It provides assurance that the home’s value meets or exceeds the amount being lent for its purchase. In most cases, a licensed appraiser will analyze the property’s condition and review the value of comparable properties that have recently sold. Mortgage borrowers are usually expected to pay the cost of an appraisal. These fees are often due upfront and non-refundable.2 Appraisal requirements can vary by lender and loan type, and in today’s market in-person appraisal waivers have become much more common. Analysis of the property, the local market, and the buyer’s qualifications will determine whether the appraisal will be waived. Not all properties or buyers will qualify, and not all mortgage lenders will utilize this system.3 If you’re applying for a mortgage, be sure to ask your lender about their specific terms. If you’re a cash buyer, you may choose—but are not obligated—to order an appraisal. APPRAISALS IN A RAPIDLY SHIFTING MARKET An appraisal contingency is a standard inclusion in a home purchase offer. It enables the buyer to make the closing of the transaction dependent on a satisfactory appraisal wherein the value of the property is at or near the purchase price. This helps to reassure the buyer (and their lender) that they are paying fair market value for the home and allows them to cancel the contract if the appraisal is lower than expected. Low appraisals are not common, but they are more likely to happen in a rapidly appreciating market, like the one we’re experiencing now.4 That’s because appraisers must use comparable sales (commonly referred to as comps) to determine a property’s value. These could include homes that went under contract weeks or even months ago. With home prices rising so quickly,5 today’s comps may be lagging behind the market’s current reality. Thus, the appraiser could be basing their assessment on stale data, resulting in a low valuation. HOW ARE BUYERS AND SELLERS IMPACTED BY A LOW APPRAISAL? When a property appraises for less than the contract price, you end up with an appraisal gap. In a more balanced market, that could be cause for a renegotiation. In today’s market, however, sellers often hold the upper hand. That’s why some buyers are using the potential for an appraisal gap as a way to strengthen their bids. They’re proposing to take on some or all of the risk of a low appraisal by adding gap coverage or a contingency waiver to their offer. Appraisal Gap Coverage Buyers with some extra cash on hand may opt to add an appraisal gap coverage clause to their offer. It provides an added level of reassurance to the sellers that, in the event of a low appraisal, the buyer is willing and able to cover the gap up to a certain amount.6 For example, let’s say a home is listed for $200,000 and the buyers offer $220,000 with $10,000 in appraisal gap coverage. Now, let’s say the property appraises for $205,000. The new purchase price would be $215,000. The buyers would be responsible for paying $10,000 of that in cash directly to the seller because, in most cases, mortgage companies won’t include appraisal gap coverage in a home loan.6 Waiving The Appraisal Contingency Some buyers with a higher risk tolerance—and the financial means—may be willing to waive the appraisal contingency altogether. However, this strategy isn’t for everyone and must be considered on a case-by-case basis. It’s important to remember that waiving an appraisal contingency can leave a buyer vulnerable if the appraisal comes back much lower than the contract price. Without an appraisal contingency, a buyer will be obligated to cover the difference or be forced to walk away from the transaction and relinquish their earnest money deposit to the sellers.7 It’s vital that both buyers and sellers understand the benefits and risks involved with these and other competitive tactics that are becoming more commonplace in today’s market. We can help you chart the best course of action given your individual circumstances. DON’T WAIVE YOUR RIGHT TO THE BEST REPRESENTATION There’s never been a market quite like this one before. That’s why you need a master negotiator on your side who has the skills, instincts, and experience to get the deal done...no matter what surprises may pop up along the way. If you’re a buyer, we can help you compete in this unprecedented market—without getting steamrolled. And if you’re a seller, we know how to get top dollar for your home while minimizing hassle and stress. Contact us today to schedule a complimentary consultation. Sources:

Learn how to determine your current net worth and how an investment in real estate can help improve your bottom line.

Among its many impacts, COVID-19 has had a pronounced effect on the housing market. Low home inventory and high buyer demand have driven home prices to an all-time high.1 This has given an unexpected financial boost to many homeowners during a challenging time. However, for some renters, rising home prices are making dreams of homeownership feel further out of reach. If you’re a homeowner, it’s important for you to understand how your home’s value contributes to your overall net worth. If you’re a renter, now is the time for you to figure out how homeownership fits into your short-term goals and your long-term financial future. An investment in real estate can help you grow your net worth, build wealth over time, and gain a foothold in the housing market to keep pace with rising prices. What is net worth? Net worth is the net balance of your total assets minus your total liabilities. Or, basically, it is what you own minus what you owe.2 Assets include the cash you have on hand in your checking and savings accounts, investment account balances, salable items like jewelry or a car and, of course, your home and any other real estate you own. Liabilities include your total debt obligations like car loans, credit card debt, the amount you owe on your mortgage, and student loans. In addition, liabilities would include any other payment obligations you have, like outstanding bills and taxes. How do I calculate my net worth? To calculate your net worth, you’ll want to add up all of your assets and all of your liabilities. Then subtract your total liabilities from your total assets. The balance represents your current net worth. Total Assets – Total Liabilities = Net Worth Ready to calculate your net worth? Contact us to request an easy-to-use worksheet and a free assessment of your home’s current market value! Keep in mind that your net worth is a snapshot of your financial position at a single point in time. Your assets and liabilities will fluctuate over both the short term and long term. For example, if you take out a loan to buy a car, you decrease your liability with each payment. Of course, the value of your asset (the car) will depreciate over time, as well. An asset that is invested in stocks or bonds can be even less predictable, as it’s subject to daily fluctuations in the market. As a homeowner, you enjoy significant stability through your monthly real estate investment, also known as your home mortgage payment. While the actual value of your home can fluctuate depending on market conditions, your mortgage payment will decrease your liability each month. And unlike a vehicle purchase, the value of your home is likely to appreciate over time, which can help to grow your net worth. Right now, your asset may be worth significantly more than it was this time last year.3 If you’re a homeowner, contact us for an estimate of your home’s market value so that you can factor it into your net worth calculation. If you’re not a current homeowner, let’s talk about how homes in our area have appreciated over the last several years. That way, you can get an idea of how a home purchase could positively affect your net worth. How can real estate increase my net worth? When you put your real estate dollars to work, it’s possible to grow your net worth, generate cash flow, and even fund your retirement. We can help you realize the possibilities and maximize the return on your investment. Property Appreciation Generally, property appreciates in one of two ways: either through changes to the overall market or through value-added modifications to the property itself.

This type of property appreciation is the one that many homeowners are enjoying right now. Buyer demand is at an all-time high due to a combination of record-low interest rates and limited housing inventory.4 At other times, rising home prices have been attributed to different factors. Certain local conditions—like a new commercial development, influx of jobs, or infrastructure project—can encourage rapid growth in a community or region and a corresponding rise in home values. Historically, home prices have been shown to experience an upward trend punctuated by intermittent booms and corrections.5 2. Strategic home improvements Well-planned and executed home improvements can also impact a home’s value and increase homeowner equity at the same time. The type of home improvement should be appropriate for the home and in tune with the desires of local buyers. For example, a tasteful exterior remodel that is in keeping with the preferences of local home buyers is likely to add significant value to a home, while remodeling the home to look like the Taj Mahal or a favorite theme park attraction will not. A modern kitchen remodel tends to add value, while a kitchen remodel that is overly expensive or personalized may not provide an adequate return on investment. Investment Property You may be used to thinking of investments primarily in terms of stocks and bonds. However, the purchase of a real estate investment property offers the opportunity to increase your net worth both upon purchase and year after year through appreciation. In addition, rental payments can have a positive impact on your monthly income and cash flow. If you currently have significant equity in your home, let's talk about how you could put that equity to work by funding the purchase of an investment property.

A long-term rental property is one that is leased for an extended period and typically used as a primary residence by the renter. This type of real estate investment offers you the opportunity to generate consistent cash flow while building equity and appreciation.6 As an owner, you don’t usually have to worry about paying the utility bills or furnishing the property—both of which are typically covered by the tenant. Add to this the fact that traditional tenants translate into less time and effort spent on day-to-day property management, and long-term rentals are an attractive option for many investors. 2. Short-term or vacation rental Short-term rentals are often referred to as vacation rentals because they are primarily geared towards recreational travelers. And as more people start to feel comfortable traveling again, the short-term rental market is poised to become a more popular option than ever. In 2020 alone, in the thick of widespread travel bans, the short-term rental platform Airbnb’s market share of the hospitality industry reached as high as 41 percent.6 Investing in a short-term rental offers many benefits. If you purchase an investment property in a top tourist destination, you can expect steady demand from travelers while taking advantage of any non-rented periods to enjoy the home yourself. You can also adjust your rental price around peak demand to maximize your cash flow while building equity and long-term appreciation. To reap these benefits, however, you’ll need to understand the local laws and regulations on short-term rentals. We can help you identify suitable markets with investment potential. WE’RE HERE TO HELP Ready to calculate your personal net worth? Contact us for an easy-to-use worksheet and to find out your home’s current value. And if you want to learn more about growing your net worth through real estate, we can schedule a free consultation to answer your questions and explore your options. Whether you’re hoping to maximize the value of your current home or invest in a new property, we’re here to help you achieve your real estate goals. The above references an opinion and is for informational purposes only. It is not intended to be financial advice. Consult the appropriate professionals for advice regarding your individual needs. Sources:

Can I Buy or Sell a Home Without a Real Estate Agent?

Today’s real estate market is one of the fastest-moving in recent memory. With record-low inventory in many market segments, we’re seeing multiple offers—and sometimes even bidding wars—for homes in the most sought-after neighborhoods. This has led some sellers to question the need for an agent. After all, why spend money on a listing agent when it seems that you can stick a For Sale sign in the yard then watch a line form around the block? Some buyers may also believe they’d be better off purchasing a property without an agent. For those seeking a competitive edge, proceeding without a buyer’s agent may seem like a good way to stand out from the competition—and maybe even score a discount. Since the seller pays the buyer agent’s commission, wouldn’t a do-it-yourself purchase sweeten the offer? We all like to save money. However, when it comes to your largest financial asset, forgoing professional representation may not always be in your best interest. Find out whether the benefits outweigh the risks (and considerable time and effort) of selling or buying a home on your own—so you can head to the closing table with confidence. SELLING YOUR HOME WITHOUT AN AGENT Most homeowners who choose to sell their home without any professional assistance opt for a traditional “For Sale By Owner” or a direct sale to an investor, such as an iBuyer. Here’s what you can expect from either of these options. For Sale By Owner (FSBO) For sale by owner or FSBO (pronounced fizz-bo) offers sellers the opportunity to price their own home and handle their own transaction, showing the home and negotiating directly with the buyer or his or her real estate agent. According to data compiled by the National Association of Realtors, approximately 8% of homes are sold by their owner.1 In an active, low inventory real estate market, it may seem like a no-brainer to sell your home yourself. After all, there are plenty of buyers out there and one of them is bound to be interested in your home. In addition, you’ll save money on the listing agent’s commission and have more control over the way the home is priced and marketed. One of the biggest problems FSBOs run into, however, is pricing the home appropriately. Without access to information about the comparable properties in your area, you could end up overpricing your home (causing it to languish on the market) or underpricing your home (leaving thousands of dollars on the table).2 Even during last year’s strong seller’s market, the median sales price for FSBOs was 10% less than the median price of homes sold with the help of a real estate agent.1 And during a more balanced market, like the one we experienced in 2018, FSBO homes sold for 24% (or $60,000) less than agent-represented properties.3 This suggests that, while you may think that you’ll price and market your home more effectively yourself, in fact you may end up losing far more than the amount you would pay for an agent’s assistance. Without the services of a real estate professional, it will be up to you to get people in the door. You’ll need to gather information for the online listing and put together the kind of marketing that today’s buyers expect to see. This includes bringing in a professional photographer, writing the listing description, and designing marketing collateral like flyers and mailers—or hiring a writer and graphic designer to do so. Once someone is interested, you’ll need to offer virtual showings and develop a COVID safety protocol. You’ll then need to schedule an in-person showing (or in some cases, two or three) for each potential buyer. In addition, you’ll be on your own when evaluating offers and determining their financial viability. You’ll need to thoroughly understand all legal contracts and contingencies and discuss terms, including those regarding the home inspection and closing process. While you’re doing all of this work, it’s likely that you’ll still need to pay the buyer agent’s commission. So be sure to weigh your potential savings against the significant risk and effort involved. If you choose to work with a listing agent, you’ll save significant time and effort while minimizing your personal risk and liability. And the increased profits realized through a more effective marketing and negotiation strategy could more than make up for the cost of your agent’s commission. iBuyer iBuyers have been on the scene since around 2015, providing sellers the option of a direct purchase from a real estate investment company rather than a traditional direct-to-consumer sales process.4 iBuyer companies tout their convenience and speed, with a reliable, streamlined process that may be attractive to some sellers. The idea is that instead of listing the home on the open market, the homeowner completes an online form with information about the property’s location and features, then waits for an offer from the company. The iBuyer is looking for a home in good condition that’s located in a good neighborhood—one that’s easy to flip and falls within the company’s algorithm. For sellers who are more focused on speed and convenience, an iBuyer may offer an attractive alternative to a traditional real estate sale. That’s because iBuyers evaluate a property quickly and make an upfront offer without requesting repairs or other accommodations. However, sellers will pay for that convenience with, generally, a far lower sale price than the market will provide as well as fees that can add up to as much or more than a traditional real estate agent’s commission. According to a study conducted by MarketWatch, iBuyers netted, on average, 11% less than a traditional sale when both the lower price and fees are considered.5 Other studies found some iBuyers charging as much as 15% in fees and associated costs, far more than you’ll pay for a real estate agent’s commission.6 In a hot market, this can mean leaving tens of thousands of dollars on the table since you won’t be able to negotiate and you’ll lose out on rising home prices caused by low inventory and increased demand. In addition, iBuyers are demonstrably less reliable during times of economic uncertainty, as evidenced by the halt of operations for most iBuyer platforms in early 2020.6 As a seller, the last thing you want is to start down the road of iBuying only to find out that a corporate mandate is stopping your transaction in its tracks. If you choose to work with a real estate agent, you can still explore iBuyers as an option. That way you can take advantage of the added convenience of a fast sale while still enjoying the protection and security of having a professional negotiating on your behalf. BUYING YOUR HOME WITHOUT AN AGENT According to the most recent statistics, 88% of home buyers use a real estate agent when conducting their home search.1 A buyer’s agent is with you every step of the way through the home buying process. From finding the perfect home to submitting a winning offer to navigating the inspection and closing processes, most homebuyers find their expertise and guidance invaluable. And the best part is that, because they are compensated through a commission paid by the homeowner at closing, most agents provide these services at no cost to you! Still, you may be considering negotiating your home purchase directly with the seller or listing agent, especially if you are accustomed to deal-making as part of your job. And if you are familiar with the neighborhood where you are searching, you may feel that there is no reason to get a buyer’s agent involved. However, putting together a winning offer package can be challenging. This is especially true in a multiple-offer situation where you’ll be competing against buyers whose offers are carefully crafted to maximize their appeal. And the homebuying process can get emotional. A trusted agent can help you avoid overpaying for a property or glossing over “red flags” in your inspection. In addition, buyer agents offer a streamlined, professional process that listing agents may be more likely to recommend to their clients. If you decide to forego an agent, you’ll have to write, submit, and negotiate a competitive offer all on your own. You’ll also need to schedule an inspection and negotiate repairs. You’ll be responsible for reviewing and preparing all necessary documents, and you will need to be in constant communication with the seller’s agent and your lender, inspector, appraiser, title company, and other related parties along the way. Or, you could choose to work with a buyer’s agent whose commission is paid by the seller and costs you nothing out of pocket. In exchange, you’ll obtain fiduciary-level guidance on one of the most important financial transactions of your life. If you decide to go it alone, you’ll be playing fast and loose with what is, for most people, their most important and consequential financial decision. SO, IS A REAL ESTATE AGENT RIGHT FOR YOU? It is important for you to understand your options and think through your preferences when considering whether or not to work with a real estate professional. If you are experienced in real estate transactions and legal contracts, comfortable negotiating under high-stakes circumstances, and have plenty of extra time on your hands, you may find that an iBuyer or FSBO sale works for you. However, if, like most people, you value expert guidance and would like an experienced professional to manage the process, you will probably experience far more peace of mind and security in working with a real estate agent or broker. A real estate agent’s comprehensive suite of services and expert negotiation skills can benefit buyers and sellers financially, as well. On average, sellers who utilize an agent walk away with more money than those who choose the FSBO or iBuyer route.3,5 And buyers pay nothing out of pocket for expert representation that can help them avoid expensive mistakes all along the way from contract to closing. According to NAR’s profile, the vast majority of buyers (91%) and sellers (89%) are thrilled with their real estate professional’s representation and would recommend them to others.1 That’s why, in terms of time, money, and expertise, most buyers and sellers find the assistance of a real estate agent essential and invaluable. QUESTIONS ABOUT BUYING OR SELLING? WE HAVE ANSWERS The best way to find out whether you need a real estate agent or broker is to speak with one. We’re here to help and to offer the insights you need to make better-informed decisions. Let’s talk about the value-added services we provide when we help you buy or sell in today’s competitive real estate landscape. Sources:

While many areas of the economy have contracted, the housing market has stayed remarkably strong. But can the good news last?

When COVID-related shutdowns began in March, real estate brokers and clients scrambled to respond to the shift. Record-low interest rates caused some lenders to call a halt to new underwriting, and homeowners debated whether or not to put their houses on the market. However, those first days of uncertainty ushered in a period of unprecedented demand in the U.S. real estate market, which ended the year with increasing average home prices (up 13.4% from the previous year) and shrinking days on market (13 fewer than in 2019).1 Now, as the spring market approaches, you may be wondering whether the good times can continue to roll on. If you’re a homeowner, should you take advantage of this opportunity? If you’re a buyer, should you jump in and risk paying too much? Below we answer some of your most pressing questions. How is today’s market different from the one that caused the 2008 meltdown? At the beginning of the pandemic, fears of an economic recession and an ensuing mortgage meltdown were top of mind for homeowners all across the country. For many buyers and sellers, the two seemed to go hand in hand, just as they did in the 2008 economic crisis. In reality, however, the conditions that led to 2008’s recession were very different from those that triggered the current downturn—and this time, the housing market is the source of much of the good news.2 This is in line with historical patterns, as housing prices traditionally hold steady in the face of recession, with homeowners staying put and investors putting their money into bricks and mortar to ride out uncertainty in the stock market. This time around, because of lessons learned in 2008, banks are better funded, homeowners are holding more accrued equity, and, crucially, much of the economic activity is focused on financial factors outside the housing market. As many industries quickly pivoted to work-from-home, early fears of widespread job loss-related foreclosures have failed to materialize. Federal stimulus payments and the Paycheck Protection Program also helped to offset some of the worst early effects of the shutdown. Are we facing a real estate bubble? A real estate bubble can occur when there is a rapid and unjustified increase in housing prices, often triggered by speculation from investors. Because the bubble is (in a sense) filled with “hot air,” it pops—and a swift drop in value occurs. This leads to reduced equity or, in some cases, negative equity conditions. By contrast, the current rise in home prices is based on the predictable results of historically low interest rates and widespread low inventory. Basically, the principle of supply and demand is working just as it’s supposed to do. In addition, experts predict a strong seller’s market throughout 2021 along with increases in new construction.3 This should allow supply to gradually rise and fulfill demand, slowing the rate of inflation for home values and offering a gentle correction where needed. Effects of low interest ratesAccording to Freddie Mac, rates are projected to continue at their current low levels throughout 2021.4 This contributes to home affordability even in markets where homes might otherwise be considered overpriced. These low interest rates should keep the market lively and moving forward for the foreseeable future. Effects of low inventoryContinuing low inventory is another reason for higher-than-average home prices in many markets.5 This should gradually ease as an aggressive vaccination rollout and continuing buyer demand drive more homeowners to move forward with long-delayed sales plans and as new home construction increases to meet demand.6 Aren’t some markets and sectors looking particularly weak? One of the big stories of 2020 was a mass exodus from attached home communities and high-priced urban areas as both young professionals and families fled to the larger square footage and wide-open spaces of suburban and rural markets. This trend was reinforced by work-from-home policies that became permanent at some of the country’s biggest companies. Speculation then turned to the death of cities and the end of the condo market. However, it appears that rumors of the demise of these two residential sectors have been greatly exaggerated. With the first vaccine rollouts, renters have begun returning to major urban centers, attracted by the sudden rise in available inventory and newly discounted rental rates.7 In addition, buyers who were previously laser-focused on a single-family home responded to tight inventory by taking a second look at condos.8 While nationwide condo prices continue to lag behind those of detached homes, they’ve still seen significant price increases and days on market reductions year over year. In addition to these improvements, the 2020 migration has spread the economic wealth to distant suburban and rural enclaves that normally don’t benefit from increases in home values or an influx of new investment. As many of these new residents set up housekeeping in their rural retreats, they’ll revitalize the economies of their adopted communities for years to come. How has COVID affected the “seasonal” real estate market? Frequently, the real estate market is seen as a seasonal phenomenon. However, the widespread shutdowns in March 2020, coming right at the beginning of the market’s growth cycle in many areas, has led to a protracted, seemingly endless “hot spring market.” While Fannie Mae’s chief economist Douglas Duncan predicts slower growth from 2020’s historic numbers, the outlook overall is positive as we embark on the 2021 spring selling cycle.9 Duncan anticipates an additional lift in the second half of 2021 as buyers return to business as usual and look to put some of their pandemic savings to work for a down payment. Thus we could be looking at another longer-than-usual, white-hot real estate market. How will a Biden administration affect the real estate market? Projected policy around housing promises to be a boost to the real estate market in many cases.10 While some real estate investors bemoan proposed changes to 1031 Exchanges, the Biden plan for a $15,000 first-time homebuyer tax credit aims to increase affordability and bring eager new home buyers into the market. In addition, Biden-proposed policy pinpoints low inventory as a primary driver of unsustainable home values and is geared toward more affordability through investments in construction and refurbishment. Overall, according to most indicators, the real estate news looks overwhelmingly positive throughout the rest of 2021 and possibly beyond. Pent-up demand and consumer-driven policies, along with a continued low-interest-rate environment and rising inventory, should help homeowners hold on to their increased equity without throwing the market out of balance. In addition, the increase in long-term work-from-home policies promises to give a boost to a wide variety of markets, both now and in the years to come. STILL HAVE QUESTIONS? WE HAVE ANSWERS While economic indicators and trends are national, real estate is local. We’re here to answer your questions and help you understand what’s happening in your neighborhood. Reach out to learn how these larger movements affect our local market and your home’s value. Sources:

5 Secrets Buyers and Sellers Must Know About Virtual Home Tours

For years now, virtual home tours have helped real estate buyers far and wide find the perfect home. From long-distance military personnel being relocated, to investors expanding their portfolio, to homeowners looking for a vacation getaway, this technology makes finding a house that’s a bit out of driving distance much easier. And for real estate agents, virtual tours have been a useful way to help buyers with their home search and to assist sellers in creatively marketing their listings. Because of the pandemic, virtual home showing options recently experienced a huge spike in popularity. One survey found that nearly 33% of recent home tour requests were for virtual tours, as compared to just 2% pre-pandemic.1 And it’s easy to see why. Buyers want to quickly find their next safe haven, one that may need to serve as their office, gym, and even classroom for months to come. And sellers want to limit the number of strangers in their home, yet still have the ability to reach enough potential buyers to get the best offer on their property. Virtual home tours are the popular thing right now, but that doesn’t automatically mean they’re the only option for your homebuying or selling experience. In this post, we’ll reveal five important secrets behind the virtual real estate scene. Read on to learn how they impact today’s home buyers and sellers. SECRET #1: Virtual Tours Have Evolved Lots of real estate professionals who had never used virtual tours before were forced to quickly adapt when the pandemic struck. Because of restrictions on time and resources, not everyone is able to create what would have been deemed a “virtual tour” last year. So instead, we’ve expanded the definition of the phrase by creating innovative new ways to show homes while keeping our clients safe and socially-distanced. Here are some terms you might come across as you explore homes with virtual tours. Traditional virtual tours use 360° Photos, which are images that allow you to see all angles of a space. These are what allow virtual tour viewers to look up, down, and all around the interior and exterior shots of a home. Using a software program, 360° photos can be stitched together to create a digital model that looks like a dollhouse. This is called a 3D Tour. Sometimes agents will also add Virtual Staging, which decorates rooms with digital furniture and accents like wallpaper or paint. Traditional virtual tours allow you to click to move from room to room in the home, but Online Walkthroughs feature the actual action of walking around. Either the seller or the agent (depending on factors such as time and safety requirements) will create a video by holding their camera or smartphone and simply moving through the home. Online Walkthroughs can be filmed in advance or happen live. If they are live, they can also be referred to as Virtual Showings or Online Open Houses. A Virtual Showing is often a scheduled, one-on-one event that mimics an in-person tour of the home, in which the agent and viewer start at the exterior and move their way through the property. If your agent offers to FaceTime or Skype you from a home you’re interested in, for example, that would be a type of Virtual Showing. In contrast, an Online Open House is more freeform, allowing more viewers to pop in and out of a group video call on apps such as Facebook or Zoom. SECRET #2: Virtual Doesn’t Mean Impersonal All these styles of virtual tours showcase the property’s details better than static photos ever could. But for a purchase as intimate as your next home, details like a new refrigerator or the size of the master closet aren’t the only deciding factors. Luckily, virtual tours are exceptional tools for personal connection. As a prospective buyer, virtual tours give you a feel for the property, inside and out, so you can easily picture yourself in the space and decide if the home’s flow and features work for your lifestyle. Live video walkthroughs with the real estate agent will give you insights on those crucial non-visual aspects, like creaky floors, super-fast internet speed, and neighborhood dynamics. Plus, you’ll be able to ask questions and get an insider’s perspective on what’s so great about the home. For sellers, if your agent recommends using a virtual tour to market your home, you could attract more buyers.2 And you can be sure that those interested buyers are still getting the up-close and personal look inside your home that will inspire their strongest offers. SECRET #3: Virtual Is Just The First Step To Safe Home Sales Even as government restrictions begin to ease in some areas, virtual tours are still recommended as a safer way to buy and sell real estate.3 Buyers don’t have to worry about exposure to anyone who previously visited the property, and sellers cut down on the foot traffic in their home. Some data even suggest that virtual tours keep agents safer as well, since they’re hosting fewer in-person showings and open houses.4 But despite the variety of virtual tours available, some buyers will still need to visit a home themselves in order to feel confident enough to submit an offer. In this situation, listing agents and sellers will work together to come up with a procedure that ensures everyone feels safe and comfortable. Some recommendations include requiring interested buyers to present a pre-qualification letter, conducting tours only by appointment and with essential parties, and asking buyers to self-disclose whether they have COVID-19 or exhibit any symptoms.3 The day of the in-person tour, agents might ask buyers to remain in their vehicle until they arrive at the property, and to wear protective gear such as face coverings and gloves. Many will provide hand sanitizer and will ask buyers to refrain from touching any surfaces in the home. Instead, the agent (or seller, prior to the buyers’ arrival) will turn on lights, open doors, and pull back curtains. Then, after everyone has left, the agent will return the home to its original state and disinfect it as needed.3 SECRET #4: The Speed of Closing Depends on Your Goals Though maybe not literally, virtual tours are opening doors for both buyers and sellers in terms of options available to them. In 2019, buyers viewed an average of 10 homes over a period of 10 weeks before submitting an offer.5 But thanks to an increased prevalence of virtual tours saving them driving time, they’re able to peek inside that number of homes in a much shorter period to make their final choice. With all this viewing activity, it makes sense that sellers whose listings feature virtual tours are receiving more offers on their properties. According to one study, virtual tours can add between two and three percent to the sales price of a home, in part because increased buyer interest has made sellers feel confident waiting for the exact right offer.2 So if you’re a buyer luxuriating in viewing homes from your couch, just remember that you’re not alone in your search. Your competition is virtually viewing the same properties you are, so it’s still important to work with your real estate agent to quickly submit a strong offer when you find the home of your dreams. And for sellers, if a speedy sale is important to you, carefully weigh that against the temptation to entertain more and more offers, which can keep your home on the market up to six percent longer.2 Your agent can help you decide the right strategy for your priorities. SECRET #5: Virtual May Not Always Be the Right Choice Creating, editing, uploading, and marketing virtual tours for a listing can be pricey. Packages through popular 3D imaging platforms like Matterport and Immoviewers can cost hundreds of dollars on their own.6 Virtual staging will further bloat a listing’s marketing budget, and then there’s the advertising dollars needed. Even seemingly inexpensive options like video call walkthroughs still require time and energy on behalf of both the seller and agent. These costs mean that a full virtual tour package might not always be the right choice for sellers. When you talk to your agent about marketing your home, it may be that an elaborate virtual tour, showing, and open house just don’t make sense. It could be that your potential buyers may not resonate with that type of marketing, that the investment-to-return ratio isn’t in your favor, or that there are more effective ways to get your listing seen by qualified buyers. Buyers, you may notice that some listings within your search parameters don’t offer virtual tours. That’s because those for-sale homes might not have needed a full virtual marketing package to entice buyers to submit offers, or those homes are better marketed through more traditional tactics. Don’t close the door on your dream home because it doesn’t have virtual events and features. Stay open-minded so you can consider the wealth of home options that fit your lifestyle, needs, and budget. ARE VIRTUAL HOME TOURS IN YOUR FUTURE? As technology develops, it will become easier and cheaper to create virtual tours. Coupled with the high demand for them, this means that virtual tour options are likely not only here to stay, but will continue to grow into a common addition to listings. If buying or selling a home is on your mind, we’d be happy to discuss how virtual tours can play a part in your real estate experience. Reach out to us today for help finding local homes for sale that have virtual tours, or to chat about if adding a virtual tour to your upcoming listing is the right fit. Sources:

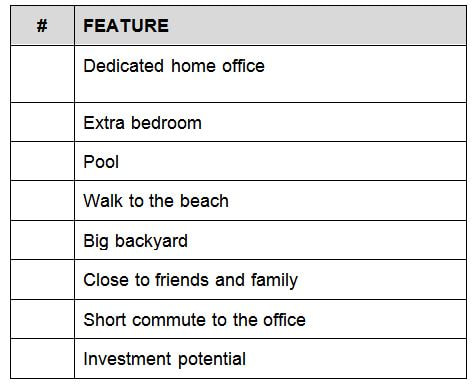

The pandemic has changed the way many of us live, work, and attend school—and those changes have impacted our priorities when it comes to choosing a home. According to a recent survey by The Harris Poll, 75% of respondents who have begun working remotely would like to continue doing so—and 66% would consider moving if they no longer had to commute as often. Some of the top reasons were to gain a dedicated office space (31%), a larger home (30%), and more rooms overall (29%).1 And now that virtual school has become a reality for many families, that need for additional space has only intensified. A growing number of buyers are choosing homes further from town as they seek out more room and less congestion. In fact, a recent survey found that nearly 40% of urban dwellers had considered leaving the city because of the COVID-19 outbreak.2 But not everyone is permanently sold on suburban or rural life. Instead, some are choosing to purchase a second home as a co-primary residence or frequent getaway. Without the requirements of a five-day commute, many homeowners feel less tethered to their primary residence and are eager for a change of scenery after spending so much time at home. If you’re feeling cramped in your current space, you’ve probably considered a move. But what type of home would suit you best: a move-up home or a second home? Let’s explore each option to help you determine which one is right for you. WHY CHOOSE A MOVE-UP HOME? A move-up home is typically a larger or nicer home. It’s a great choice for families or individuals who simply need more space, a better location, or want features their current home doesn’t offer—like an inground pool, a different floor plan, or a dedicated home office. Most move-up buyers choose to sell their current home and use the proceeds as a downpayment on their next one. If you’re struggling with a lack of functional or outdoor space in your current home, a move-up home can greatly improve your everyday life. And with mortgage rates at their lowest level in history, you may be surprised how much home you can afford to buy without increasing your monthly payment.3,4 To learn more about mortgage rates, contact us for a free copy of our recent report! “Lowest Mortgage Rates in History: What It Means for Homeowners and Buyers” One major benefit of choosing a move-up home is that you can typically afford a nicer place if you spend your entire budget on one property. However, if you’re longing for that vacation vibe, a second home may be a better choice for you. WHY CHOOSE A SECOND HOME? Once reserved for the ultra-wealthy, second homes have become more mainstream. Home sales are surging in many resort and bedroom communities as city dwellers search for a place to escape the crowds and quarantine in comfort.5 And with air travel on hold for many families, some are channeling their vacation budgets into vacation homes that can be utilized throughout the year. A second home can also be a good option if you’re preparing for retirement. By purchasing your retirement home now, you can lock in a low interest rate, start paying down the mortgage, and begin enjoying the perks of retirement living while you’re still fit and active. Plus, it’s easier to qualify for a mortgage while you’re employed, although you may be charged a slightly higher interest rate than on a primary home loan.6 One advantage of choosing a second home is that you can offset a portion of the costs—and in some cases turn a profit—by renting it out on a platform like Airbnb or Vrbo. However, be sure to consult with a real estate professional or rental management company to get a realistic sense of the property’s true income potential. WHICH ONE IS RIGHT FOR ME? You may read this and think: I’d really like both a move-up home AND a second home! But if you’re dealing with a limited budget (aren’t we all?), you’ll probably need to make a choice. These three tactics can help you decide which option is right for you. 1. Determine Your Time and Financial Budget You may meet the bank’s qualifications to purchase a home, but do you have the time, energy, and financial resources to maintain it? This is an important question to ask yourself, no matter what type of home you choose. Most buyers realize that a second home will mean double mortgages, utilities, taxes, and insurance. But consider all the extra time and expense that goes into maintaining two properties. Two lawns to mow. Two houses to clean. Two sets of systems and appliances that can malfunction. Second homes aren’t always a vacation. Make sure you’re prepared for the labor and carrying costs that go into maintaining another residence. Of course, some move-up homes require more work than a second home. For example, if your move-up option is a major fixer-upper, you’ll probably invest more energy and capital than you would on a small vacation condo by the beach. Have an honest discussion about how much time and money you want to spend on your new property. Would a move-up home or a second home be a better fit given your parameters? 2. Rank Your Priorities If you’re still undecided, make a wish list of the characteristics you’d like in your new home. Then rank each item from most to least important. This exercise can help you determine your “must-have” features—and which ones you may need to sacrifice or delay. Here’s a sample to help you get started:  3. Explore Your Options

Once you’ve determined your parameters and priorities, it’s time to begin your home search. If you’re still not sure whether a move-up home or a second home is right for you, we can help. Contact us to schedule a free consultation. We’ll discuss your options and help you assess the pros and cons of each, given your unique circumstances. We can also send you property listings for both move-up homes and second homes within your budget so you can better envision each scenario. Sometimes, viewing listings of homes that meet your criteria can make the decision clear. LET’S GET MOVING Whether you’re ready to make a move or need help weighing your options, we’d love to help. We can determine your current home’s value and show you local properties that fit within your budget. Or, if your heart is set on a second home in another market, we can refer you to an agent in your dream locale. Contact us today to schedule a free, no-obligation consultation! Sources:

Whether you’re prepping your house to go on the market or looking for ways to maximize its long-term appreciation, these nine home improvement projects are great ways to add function, beauty, and real value to your home.

The best part is, once you’ve secured the materials, most of these renovations can be completed over the course of a weekend. And they don’t require a lot of specialized skills or experience. So grab your toolbox, then get ready to boost your home’s appeal AND investment potential! 1. Spruce Up Your Landscaping Landscaping improvements can increase a home’s value by 10-12%.1 But which outdoor features do buyers care about most? According to a survey of Realtors, a healthy lawn is at the top of their list. If your lawn is lacking, overseeding or laying new sod can be a worthwhile investment—with an expected return of 417% and 143% respectively.1 Planting flowers is another great way to enhance your home’s curb appeal. And if you choose a perennial variety, your blooms should return year after year. For an even longer-term impact, consider planting a tree. According to the Council of Tree and Landscape Appraisers, a mature tree can add up to $10,000 to the value of your home.2 2. Clean The Exterior When it comes to making your house shine, a sparkling facade can be just as important as a clean interior. Real estate professionals estimate that washing the outside of a house can add as much as $15,000 to its sales price.3 A rented pressure washer from your local home improvement store can help you remove built-up dirt and grime from your home’s exterior, walkway, and driveway. Just be sure to read the instructions carefully—and only use it on surfaces that can withstand the intensity. When in doubt, a scrub brush and bucket of sudsy water will often do the trick. 3. Add A Fresh Coat Of Paint New paint can have a big impact on both the appearance and value of a property. In fact, it’s one of the most effective ways to revitalize a home’s exterior, update its interior, and make it appear larger and brighter. The best part? Painting is relatively easy and inexpensive! To get the maximum return at resale, stick with a modern but neutral color palette that will appeal to a broad range of buyers. According to a recent survey of home design experts, cool neutrals are a safe bet when it comes to interior paint. And respondents chose white and gray as the best exterior paint colors to use when selling a home.4 However, it’s important to consider a property’s architecture, existing fixtures, and regional design preferences, as well. 4. Install Smart Home Technology In a recent survey, 78% of real estate professionals said their buyer clients were willing to pay more for a home with smart technology features.5 The most requested smart devices? Thermostats (77%), smoke detectors (75%), home security cameras (66%), and locks (63%).6 The good news is, many of these gadgets are fairly easy to install. And some of them, including smart thermostats and light bulbs, will pay for themselves over time by making your home more energy efficient. In fact, many manufacturers report that smart thermostats can cut back on heating and cooling costs by 10-20%.7 If you already own a smart speaker, like Amazon Alexa or Google Home, choose devices that will pair with your existing technology. This will enable you to create a truly integrated (and in many cases voice-activated) smart home experience. 5. Modernize Your Window Treatments Smart—or motorized—blinds are also growing in popularity, and several manufacturers make models you can order and install on your own. But they’re not the only way to modernize your window treatments. If you have old aluminum blinds, consider replacing them with plantation shutters, which are energy efficient, durable, and have strong buyer appeal.8 Roman and roller shades are another stylish alternative, and they come in a variety of colors and fabrics, which you can personalize to meet your design and privacy preferences. Fortunately, upgrading your blinds has gotten easier and less expensive in recent years. There are a number of retailers that specialize in affordable window coverings that are simple to measure and hang yourself. 6. Replace Outdated Fixtures Drastically transform the look and feel of your home by swapping out dingy and dated fixtures for contemporary alternatives. Start by assessing your current light fixtures, faucets, cabinet hardware, door knobs, and even switch plates. Then prioritize replacing those that are particularly outdated or in highly-visible areas, such as your entryway or kitchen. Even if your home is fairly new, consider trading your builder-grade fixtures for higher-end options to give it a more upscale appearance. And forget the old rule about sticking to one metal tone throughout your property. According to designers, mixing metal finishes can add interest and character to a space.9 For more designer insights and decor trends, contact us for a free copy of our recent report: “Top 5 Home Design Trends for a New Decade.” 7. Upgrade Your Bathroom Mirror A minor bathroom remodel offers one of the best returns on investment, with a $1.71 increase in home value for every $1 you spend.10 We’ve already explored several improvements you can make to your bathroom: new paint, fixtures, and hardware. Now complete the look by upgrading your vanity’s mirror. Before you purchase a new mirror, examine your existing one to see how it is attached to the wall. Some vanity mirrors are glued to the wall and difficult to remove without shattering the glass or damaging the sheetrock behind it.11 If you prefer to keep your existing mirror, you can paint the frame—or add one if it’s currently frameless. There are several online retailers that will send you the frame components cut to your specifications, which you can assemble and mount yourself. Much like a work of art, your vanity mirror serves as a focal point for your bathroom, so let your creativity shine through! 8. Shampoo Your Carpet Carpet is notorious for trapping dust, dirt, and allergens. It’s one of the reasons that most buyers prefer hard surface flooring.12 But if you love your carpet, or you’re not ready to invest in an alternative, make an effort to keep it clean and odor-free. To properly maintain your carpet, you should vacuum it weekly. Experts also recommend a deep shampoo at least every two years.13 Fortunately, this is a cheap and easy DIY project you can knock out in about 20 minutes per room. According to Consumer Reports, you can rent a machine and purchase cleaning fluid and supplies for around $90. With an average return on your investment of 169%, it’s well worth the effort and expense.14 9. Customize Your Closet Real estate professionals estimate that a closet remodel can add $2500 to a home’s selling price. And while a professional renovation can cost upwards of $6000, there are many high-quality DIY closet systems you can customize and install yourself.15 Experts recommend taking a thorough inventory of your wardrobe and accessories before you get started. Make sure frequently-worn pieces are easy to reach, and store seasonal and seldom-used items on high shelves. Place shoe racks near the closet entrance so they are easy to access.16 A little planning can go a long way toward building a closet that you (and your future buyers!) will love. GET A COMPLIMENTARY ANALYSIS OF YOUR PROJECT We’ve been talking averages. But the truth is, the actual impact of a home improvement project will vary depending on your particular home and neighborhood. Before you get started, contact us to schedule a free virtual consultation. We can help you determine which upgrades will offer the greatest return on your effort and investment. Sources:

|

Real Estate Broker

Silicon Valley Real Estate Guy Archer Rock Properties (408) 569-9000 ClaytonYoung@gmail.com CalBRE#01768240 *Extraordinary Service

*Trust *Integrity *Amazing Results |